Accredited real estate investors eager to graduate from the do-it-yourself approach into more passive arrangements may be familiar with real estate syndication structures.

These entities, often established as limited partnerships (LPs) or limited liability companies (LLCs), allow anywhere from two to several hundred (or even thousands of) investors to pool their capital and talents together to purchase or invest in much larger properties than they could otherwise afford when investing alone.

How Do Real Estate Syndication Structures Work?

Syndications involving family members, relatives, friends, and other closely-related investors may occasionally function democratically. In these partnerships, each participant contributes both time and labor in addition to capital, and all syndicate members play an active role in sourcing, developing, buying, renovating, leasing, and/or selling real estate.

Who Does the Work in a Real Estate Syndicate?

In most syndication structures, however, investors delegate both the day-to-day work and the authority to make decisions to a general partner (GP), who is responsible for finding deals, performing due diligence, obtaining financing, and managing properties on behalf of the syndicate. GPs who lead syndicates that invest in ground-up construction or properties requiring rehabilitation will be tasked with overseeing those activities.

What about the remaining members of the syndicate? Known as limited partners (LPs), these participants enjoy a fully hands-off approach to real estate investing. At the same time, LPs receive a predetermined share of the syndicate’s cash flow and capital gains—the former from rents earned by real estate investments owned by the syndicate and the latter from property appreciation which may be realized in a sale or refinance..

How Are Profits Earned by the Syndicate Distributed?

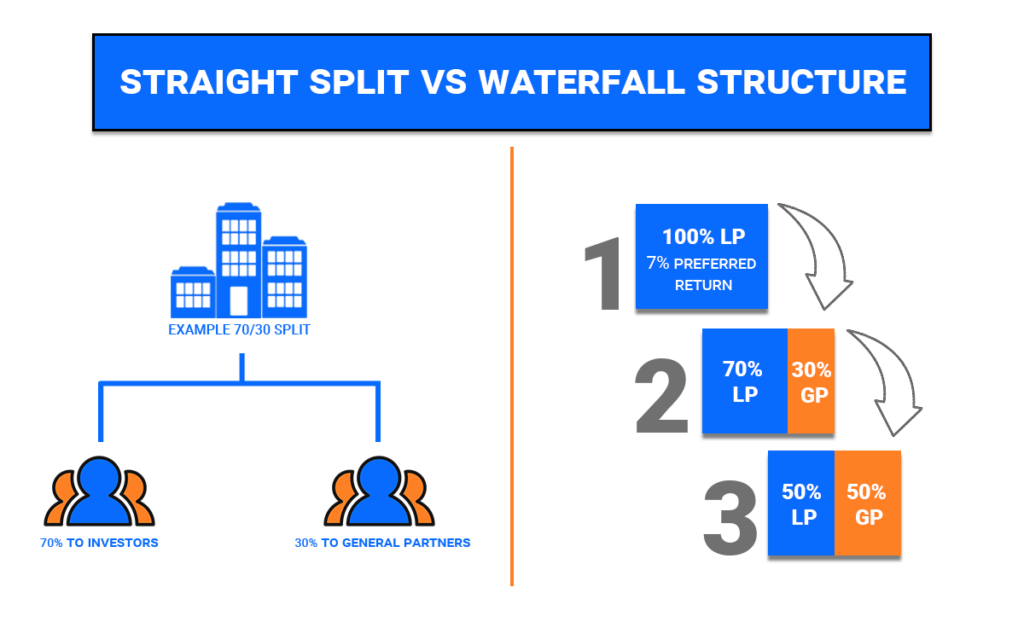

GPs are often paid an asset management fee and promoted interest as compensation for leading the syndicate. Colloquially known as a “promote”, this fee entitles the GP to a disproportionate share of the syndicate’s profits above a hurdle rate which is predetermined.

Many ask, what’s in it for LPs? Beyond the benefit of a completely passive real investing experience, LPs often have an option of a preferred return, which is identical to the GP’s hurdle rate. This means that LPs receive 100% of the profits earned by the syndicate up to the preferred return, and thus are first in line to receive the syndicate’s assets and profits.

Notably, if a syndicate does not eclipse the hurdle rate, the GP receives no promoted profit and only earns an asset management fee if that.

From a downside perspective, LPs also bear less risk than the GP. While an LP’s maximum liability is limited to the amount they invested in the syndicate—that is, they can’t lose any more than they put in—the GP faces unlimited liability. In other words, a GP’s personal assets may be exposed to claims from creditors if a deal underperforms significantly enough.

What Decisions Do a Syndicate’s Limited Partners Get To Make?

Beyond contributing the initial capital, LPs do not participate in the syndicate’s operations and are not involved in strategic decisions concerning financing or dealmaking.

There is a key benefit in deliberately remaining a passive investor: If LPs assume too active of a role in the syndicate, they may have to sign personal guarantees and thus assume unlimited liability for the syndicate’s debts.

Some syndicates are nonetheless structured in a way that requires the GP to obtain approval from LPs for major decisions. In these arrangements, LPs retain limited liability but function as an advisory committee to the GP, where they have the right to vote on resolutions such as whether or not to assume debt beyond a certain leverage ratio or dispose of a currently-owned investment property.

Can Limited Partners Choose Which Properties to Invest In?

Before investing, LPs receive information about the syndicate’s investment philosophy and target market .

This information provides LPs with a general understanding of the syndicate’s business plan and investment offerings—including factors like the asset class (multifamily, office, medical, industrial, etc.), geography (primary, secondary, tertiary, small town, or rural market), quality (class A, B, or C), and others.

However, GPs often raise money from LPs before identifying a deal (or deals), meaning that neither the LPs nor the GP will know what specific investments the syndicate will make ahead of time.

Single-Deal Syndicates Let LPs Pick and Choose Deals.

Other times, a syndicate’s GP may have already identified a deal prior to raising money from LPs. If this is the case, details about the specific offering—like its address, footprint, unit count, income history, asking price, estimated total capitalization, forecasted holding period, and projected IRR—will be shared in the private placement memorandum (PPM) issued to LPs during the onboarding process.

These partnerships are known as single-deal syndicates, allowing prospective LPs to decide whether they want to invest in the property brought forward by the GP before committing any capital to the syndicate.

If LPs bring enough capital to the table to close the deal, the syndicate acquires the target property, improves it and/or holds it for cash flow, and then sells it after a predetermined holding period. Once the syndicate disposes of the property, LPs and the GP are paid out, and the entity winds down.

Can Limited Partners Invest in Multiple Single-Deal Syndicates?

Though single-deal syndicates only invest in one specific property, LPs who want exposure to multiple properties are welcome to participate in more than one single-deal syndicate at a time.

So long as LPs meet the minimum investment requirements for each syndicate and feel comfortable contending with varying holding periods, fee structures, and terms, LPs may invest in as many single-deal syndicates—or evergreen syndicates, for that matter—as they wish.

How Long Do Single-Deal Syndicates Last?

Since each opportunity identified by a single-deal syndicate is unique, no two syndicates are alike, so it’s hard to offer an exact answer.

Generally, single-deal syndicates seek to capture short-term opportunities and thus feature relatively shorter holding periods that often range between 2 and 5 years. That said, some funds may hold their properties for seven years or longer.

LPs seeking information about their specific syndicate’s holding period should consult the PPM or contact their GP.

What Kinds of Real Estate Do Single-Deal Syndicates Buy?

Across the industry, single-deal syndicates target properties that run the gamut from office buildings and industrial warehouses to strip malls and multifamily buildings.

Across the industry, single-deal syndicates target properties that run the gamut from office buildings and industrial warehouses to strip malls and multifamily buildings.

That said, GPs run real estate private equity (REPE) firms that usually specialize in one asset class or geographic area, so it’s not uncommon for their single-deal syndicates to feature properties from just one particular category.

Veloce Capital specializes in multifamily real estate, our single-deal syndicates provide investors with ground-up developments of different sizes, and have redevelopment equity and distressed assets leveraging rental income.

Single-Deal Syndication Offerings for Alternative Investors

With experience structuring over $1 billion in real estate transactions and a decade-long track record of delivering double-digit returns for investors, Veloce Capital is one of the northeastern United States’ fastest-growing multifamily real estate private equity firms.

LPs who partner with Veloce Capital unlock access to several unique investment structures. Our single-deal syndicates give investors the freedom to pick and choose specific properties without forgoing the benefits of a fully-passive approach to alternative real estate investing. At the same time, our multifamily equity and debt funds follow an evergreen strategy and benefit from the ongoing deal flow. And through our subscription fund, even non-accredited investors can get involved—a rarity in the REPE space.

Find a moment to speak with us today to see if becoming an LP in our single-deal syndicates can help you earn risk-adjusted returns.